For Business & Service Inquiries

Sales Team

Project quotes, partnerships, implementation

U.S. financial institutions lost over $485 billion to fraud in 2023, and that number has continued climbing. At the same time, customers expect their bank or insurer to know them personally—to anticipate needs, resolve issues instantly, and deliver seamless digital experiences. Meanwhile, fintech startups are capturing market share by moving faster and operating leaner than most legacy institutions can match.

Add tightening regulatory requirements and relentless pressure to cut operational costs, and it's clear why BFSI leaders are reassessing their technology strategies from the ground up.

AI is no longer a future investment for BFSI organizations. It has become a strategic necessity.

The global AI in BFSI market is projected to surpass $130 billion by 2030, growing at a compound annual rate exceeding 30%. Leading U.S. banks, insurers, and investment firms are already deploying AI at scale—not as experiments, but as core infrastructure.

This article walks you through exactly how they're doing it, what results they're achieving, and how your organization can build a practical path forward.

Quick Reference for BFSI AI Decision-Makers

- AI in BFSI refers to deploying machine learning, generative AI, and intelligent automation to improve fraud detection, compliance, customer service, and risk management across banking, financial services, and insurance.

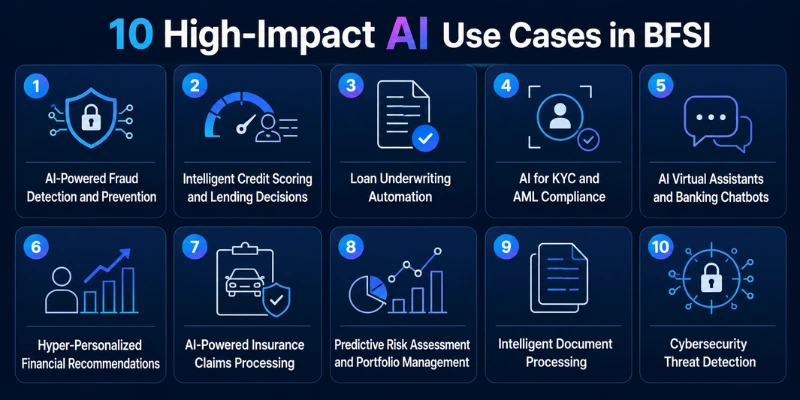

- The top 10 AI use cases in BFSI include fraud detection, credit scoring, KYC/AML automation, virtual assistants, claims processing, and cybersecurity threat detection.

- U.S. financial institutions using AI report significant reductions in fraud losses, faster loan processing, and measurable improvements in customer satisfaction scores.

- AI implementation costs vary widely—from $50,000 for targeted chatbot deployments to $5M+ for enterprise-wide AI ecosystems—depending on scope, data readiness, and compliance requirements.

- Successful AI adoption in BFSI requires a clear business case, high-quality data infrastructure, regulatory alignment, and a technology partner with proven BFSI experience.

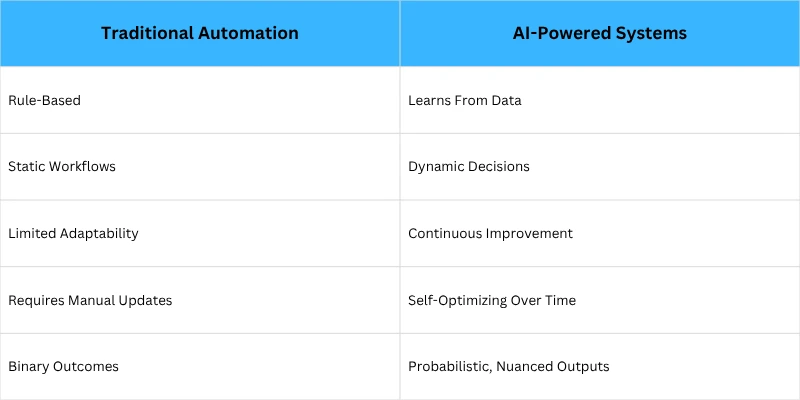

AI in BFSI is the application of machine learning, deep learning, natural language processing, generative AI, and predictive analytics to automate decisions, detect patterns, and create personalized experiences across banking, financial services, and insurance.

It goes far beyond rule-based automation. Traditional systems follow fixed instructions. AI systems learn from data, adapt over time, and make probabilistic decisions that improve with experience.

Key technologies powering AI in BFSI include:

Few industries are better positioned to benefit from AI than BFSI—and few generate more data to fuel it.

Financial institutions process millions of transactions daily. Every payment, loan application, insurance claim, and customer interaction produces structured data that AI systems can analyze in real time.

Beyond data volume, BFSI has three additional accelerants:

The bottom line: traditional automation executes. AI thinks, learns, and improves.

Several pressures are converging to make AI adoption not just attractive but urgent.

Fraud losses are accelerating. Synthetic identity fraud, account takeover attacks, and real-time payment fraud are outpacing traditional detection systems. AI can identify anomalies across thousands of variables simultaneously—something no rule-based system can match.

Cybersecurity threats are growing in sophistication. Ransomware, phishing attacks, and insider threats now target financial institutions more aggressively than ever. AI-driven threat detection responds in milliseconds, not hours.

Customers demand personalization. A McKinsey study found that personalization at scale can increase bank revenues by 10–15%. AI enables that at a level no human advisory team can replicate alone.

Regulatory pressure is intensifying. The OCC, FDIC, and CFPB are expanding oversight of AI use in lending and compliance—but also pushing institutions to modernize their risk and reporting infrastructure. AI helps on both fronts.

Fintech disruption is real. Companies like Chime, SoFi, and Betterment are winning customers by offering faster, smarter, more personalized financial products. Institutions working with fintech application builders to develop their own AI-powered products are closing the competitive gap.

Cost optimization is non-negotiable. Labor-intensive processes like loan processing, document review, and customer onboarding are expensive. AI dramatically reduces per-transaction costs while improving accuracy.

What it is: Real-time identification of fraudulent transactions, accounts, and behaviors using machine learning models trained on historical fraud data.

How it works: AI monitors every transaction as it happens, scoring it for fraud risk based on hundreds of behavioral signals—location, device, transaction history, spending velocity, and more. Anomalies trigger instant alerts or automatic blocks.

Business impact: Institutions using AI-powered fraud detection report false positive rates dropping by 50–70%, while fraud catch rates improve significantly.

Real-world example: Mastercard's Decision Intelligence platform uses AI to analyze billions of transactions annually, identifying fraud patterns that traditional systems miss entirely.

Benefits: Reduced fraud losses, fewer false declines (which frustrate legitimate customers), lower manual review costs, and faster resolution.

Future potential: AI models will increasingly combine behavioral biometrics, device intelligence, and network analysis to catch sophisticated synthetic identity fraud before accounts are even opened.

What it is: AI-driven credit assessment that goes beyond traditional FICO scores to evaluate a broader set of financial signals.

How it works: Machine learning models analyze bank transaction history, payment behavior, employment patterns, and alternative data sources to generate more accurate creditworthiness assessments.

Business impact: Financial institutions extend credit to more qualified borrowers who would have been declined by traditional scoring—while reducing default rates.

Real-world example: Upstart, a lending platform partnered with dozens of U.S. banks, uses AI to approve borrowers traditional models reject, while maintaining default rates below industry averages.

Benefits: Expanded lending reach, reduced bias in decision-making, faster approvals, and lower credit losses.

Future potential: AI models will incorporate real-time financial health data through open banking APIs, making credit assessments truly dynamic.

What it is: AI-accelerated analysis of loan applications, supporting documentation, and risk factors to streamline underwriting decisions.

How it works: AI extracts and validates data from income statements, tax returns, bank statements, and property records—then scores applications against risk models in minutes rather than days.

Business impact: Mortgage and commercial loan processing times that once took 30–45 days are being compressed to under a week.

Real-world example: Wells Fargo and several regional banks now use AI-assisted underwriting platforms that process document packages and flag missing information automatically.

Benefits: Faster time-to-close, lower per-loan processing costs, consistent underwriting standards, and improved borrower experience.

Future potential: Autonomous underwriting systems will handle routine applications end-to-end, with human review reserved for complex or high-risk cases.

What it is: AI systems that automate customer identity verification, risk screening, and anti-money laundering transaction monitoring.

How it works: AI scans identity documents, cross-references watchlists, analyzes transaction patterns for money laundering signals, and generates suspicious activity reports with supporting evidence.

Business impact: Banks spend over $25 billion annually on AML compliance in the U.S. AI can cut those costs significantly while improving detection rates.

Real-world example: HSBC partnered with an AI firm to deploy machine learning for AML monitoring, reporting a reduction in false positives—previously consuming enormous investigator time.

Benefits: Faster onboarding, lower compliance costs, fewer regulatory penalties, and better detection of sophisticated laundering schemes.

Future potential: AI will provide continuous, real-time KYC re-verification rather than periodic reviews—making compliance an ongoing process rather than a checkpoint.

What it is: Conversational AI tools that handle customer inquiries, transactions, and financial guidance across digital channels.

How it works: Large language models power chatbots that understand natural language, access account data, and complete tasks—from balance inquiries to payment processing and financial advice.

Business impact: Banks deploying AI virtual assistants report customer service cost reductions of 25–40% while handling millions more interactions without adding headcount.

Real-world example: Bank of America's Erica has handled over 1.5 billion client interactions, helping customers with spending insights, transaction searches, and proactive financial guidance.

Benefits: 24/7 availability, consistent service quality, reduced call center volume, and better data capture for personalization.

Future potential: The next generation of banking AI will move beyond question-answering to proactive financial coaching. Organizations that want to build smart AI agents capable of autonomous financial action are already investing in agentic AI architectures.

What it is: AI systems that analyze customer financial behavior and proactively surface relevant products, advice, and alerts.

How it works: ML models segment customers by financial behavior, life stage, and risk profile—then trigger personalized offers, savings nudges, investment suggestions, or debt consolidation advice at the right moment.

Business impact: Personalization-driven cross-selling increases product adoption rates by 20–30% compared to generic campaigns.

Real-world example: Capital One uses AI to surface personalized credit card offers and spending insights within its mobile app—driving measurable increases in card activation and usage.

Benefits: Higher customer lifetime value, stronger engagement, lower marketing costs, and more relevant product placement.

Future potential: AI will deliver real-time financial coaching at scale, functioning as a personalized CFO for every customer.

What it is: Automated assessment, validation, and settlement of insurance claims using computer vision, NLP, and predictive modeling.

How it works: AI analyzes claim submissions, photos, repair estimates, and historical data to validate claims, detect fraud, and calculate settlements—often in minutes.

Business impact: Insurers using AI in claims report settlement cycle times dropping from weeks to hours for straightforward claims.

Real-world example: Lemonade's AI model, Jim, processes some claims in under three seconds—reviewing the claim, running fraud checks, and issuing payment without human involvement.

Benefits: Faster claim resolution, lower claims handling costs, improved fraud detection, and higher customer satisfaction.

Future potential: Continuous claims monitoring using IoT sensor data will allow insurers to assess damage and initiate claims before customers even file.

What it is: AI systems that analyze market conditions, economic signals, and portfolio composition to optimize risk-adjusted returns.

How it works: Machine learning models process thousands of variables—market data, macroeconomic indicators, credit conditions, geopolitical signals—to forecast portfolio risk and recommend rebalancing.

Business impact: AI-driven portfolio management consistently outperforms static allocation models in volatility management.

Real-world example: BlackRock's Aladdin platform manages risk for portfolios worth over $20 trillion, using AI to model risk exposures across asset classes.

Benefits: Better risk-adjusted returns, faster response to market shifts, more consistent investment governance, and scalable portfolio oversight.

Future potential: AI will enable real-time portfolio stress testing against live market conditions, replacing periodic manual reviews.

What it is: AI extraction, classification, and validation of data from unstructured financial documents at scale.

How it works: Computer vision and NLP extract key data from contracts, regulatory filings, KYC documents, loan applications, and financial statements—routing information to the right systems automatically.

Business impact: Document processing that once required large back-office teams can now run with minimal human intervention, reducing costs and errors simultaneously.

Real-world example: JPMorgan Chase's COIN (Contract Intelligence) platform reviews commercial loan agreements in seconds, work that previously consumed 360,000 hours of lawyer time annually.

Benefits: Faster document turnaround, lower error rates, reduced manual labor costs, and better audit trails.

Future potential: AI will handle real-time regulatory document monitoring—flagging compliance issues as documents are created rather than during post-hoc audits.

What it is: AI-powered monitoring of network activity, user behavior, and transaction patterns to detect and respond to security threats in real time.

How it works: Behavioral AI establishes baselines for normal activity, then flags deviations that indicate credential theft, insider threats, or external attacks—triggering automated responses before damage occurs.

Business impact: Financial institutions using AI-driven security operations reduce average breach detection time from months to hours.

Real-world example: Citibank and other major U.S. banks have deployed AI-based security platforms that monitor billions of events daily, automatically isolating compromised endpoints.

Benefits: Faster threat response, lower breach costs, reduced analyst fatigue, and continuous 24/7 monitoring without proportional staffing increases.

Future potential: AI will increasingly predict attacks before they happen by analyzing threat intelligence feeds and identifying early attack indicators.

Building AI for banking, insurance, or financial services isn't like building AI for retail or healthcare. The stakes are higher. The regulations are stricter. The data is more sensitive. And the tolerance for error is lower.

SISGAIN works with BFSI enterprises to design and deploy custom AI solutions built from the ground up for financial services environments. Every solution is architected with enterprise-grade security, compliance-first design, and the scalability your organization needs to grow without rebuilding.

Whether you need a targeted solution for fraud detection or a comprehensive AI transformation roadmap, our skilled AI developers for your industry bring the domain knowledge to make it work—and the engineering rigor to make it last.

Our High-Impact Machine Learning Solutions are designed specifically for regulated industries where accuracy, explainability, and security aren't optional.

Schedule a Free AI Strategy Consultation →

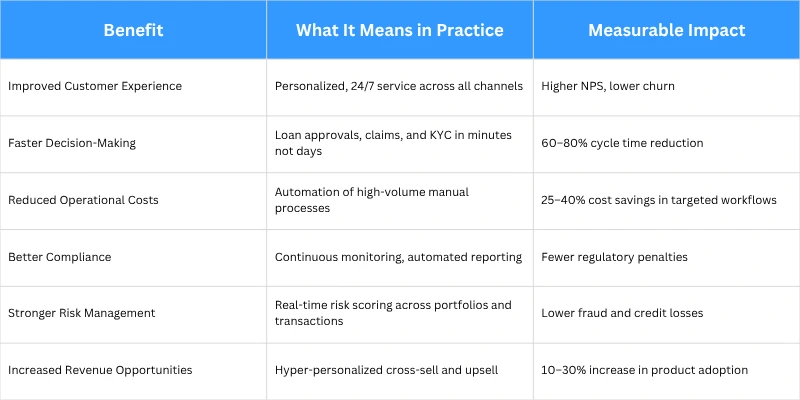

The benefits of AI in BFSI compound over time. Early adopters gain competitive advantages that become harder to close the longer peers wait.

JPMorgan Chase has invested over $18 billion annually in technology, with AI central to initiatives spanning fraud prevention, document processing, risk management, and customer experience. Its COIN platform processes loan agreements in seconds. Its AI-powered trading systems execute complex strategies with precision no human team could match at scale.

Bank of America's Erica virtual assistant has become one of the most successful AI deployments in consumer banking—not because it's technically impressive, but because it solves real customer problems. Erica proactively alerts customers to duplicate charges, upcoming bills, and unusual spending patterns.

Capital One treats itself as a technology company that happens to have a banking license. Its AI capabilities span credit decisioning, fraud detection, and hyper-personalized customer engagement. The result is one of the highest customer satisfaction scores among major U.S. card issuers.

Key lesson: The most successful banking AI deployments start with a specific problem worth solving—not a technology looking for an application.

Progressive uses AI-powered telematics through its Snapshot program to price auto insurance based on actual driving behavior rather than demographic proxies. This rewards safe drivers and improves loss ratios simultaneously.

Allstate has deployed AI across claims processing, fraud detection, and underwriting—reducing claims cycle times and identifying fraudulent claims earlier in the review process.

Key lesson: Insurance AI works best when it improves the accuracy of risk assessment, not just the speed of processing.

Robo-advisors like Betterment and Wealthfront now manage over $50 billion in combined assets using AI-driven portfolio construction and tax-loss harvesting. They've democratized investment management that was previously accessible only to high-net-worth clients.

Portfolio optimization at institutional scale—as practiced by firms like Two Sigma and Renaissance Technologies—uses AI to identify market inefficiencies and manage risk exposures in real time.

Key lesson: AI in investment management scales expertise. One AI model can serve a million investors as effectively as it serves one.

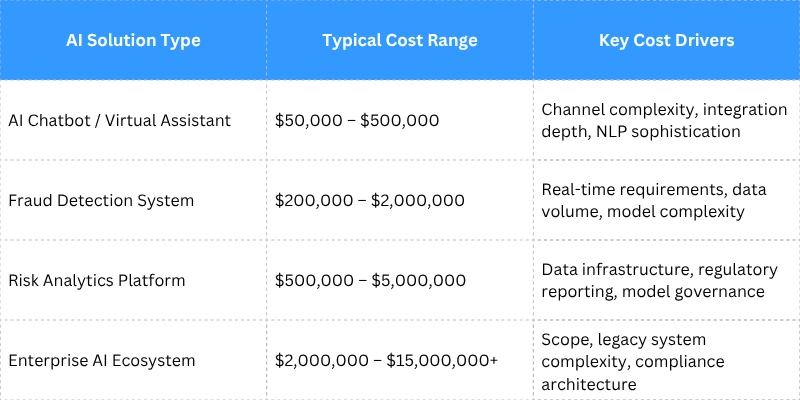

How much does AI implementation cost in BFSI? The honest answer: it depends heavily on scope, data readiness, and regulatory requirements. Here's a realistic framework.

Four factors dominate cost more than any others:

Working with a hiring Software development firm that understands BFSI-specific constraints is the most reliable way to control costs without cutting corners on compliance. Experienced fintech application builders who've navigated regulatory environments across multiple institutions bring institutional knowledge that saves time and reduces risk.

AI adoption in BFSI isn't without friction. Here are the most common challenges—and how leading institutions are addressing them.

Data privacy and security: Financial data is among the most sensitive in existence. AI systems must be designed with data minimization, encryption, and access controls built in from day one—not bolted on after deployment.

Mitigation: Adopt a privacy-by-design architecture. Use federated learning where possible to train models without centralizing sensitive data.

Regulatory compliance: The OCC, FDIC, and state regulators are increasingly focused on AI governance, model risk management, and fair lending compliance. MRM frameworks (Model Risk Management) now cover AI.

Mitigation: Build explainability and audit trails into every AI model. Engage compliance teams from the design phase, not post-deployment.

Legacy system integration: Most large banks and insurers run on core systems built decades ago. Integrating modern AI requires middleware, APIs, and significant engineering work.

Mitigation: Use API-first integration strategies and containerized AI microservices that can connect to legacy infrastructure without replacing it.

Explainability: Regulators and customers increasingly expect to understand why an AI system made a specific decision—particularly for credit, insurance pricing, or fraud flags.

Mitigation: Prioritize interpretable models (like gradient boosted trees) for high-stakes decisions. Use explainability tools like SHAP or LIME where black-box models are necessary.

AI bias: Models trained on historical data can perpetuate historical biases—particularly in lending and insurance pricing.

Mitigation: Build bias testing into model validation processes. Monitor model outputs for disparate impact across protected classes continuously.

Workforce adoption: AI changes job roles. Employees who feel threatened by AI resist it—slowing adoption and limiting returns.

Mitigation: Frame AI as augmentation, not replacement. Invest in training programs that help employees work effectively alongside AI systems.

Start with the business problem, not the technology. What specific outcome are you trying to improve? Fraud losses? Loan processing time? Customer satisfaction scores? Clear objectives drive better technology decisions—and give you a baseline to measure ROI.

Prioritize AI use cases by two dimensions: business impact and implementation feasibility. Fraud detection and document processing typically offer fast returns with manageable complexity. Start there before tackling enterprise-wide transformations.

AI is only as good as the data it learns from. Audit your data for completeness, accuracy, and accessibility. Identify gaps early. Build or improve data pipelines that can feed AI systems reliably. This step is often underestimated—and often determines whether a deployment succeeds or stalls.

This is where many BFSI AI projects succeed or fail. Choosing a partner without BFSI-specific experience creates compliance risk, integration delays, and suboptimal models. Organizations evaluating AI initiatives often seek custom AI model development providers with proven expertise in highly regulated sectors such as fintech and healthcare. Industry-focused AI partners can accelerate implementation while ensuring compliance, performance, and long-term scalability.

Deploy a limited pilot in a controlled environment before scaling. Define success metrics upfront. A 90-day pilot with clear KPIs gives you real-world validation without enterprise-wide risk. Use pilot learnings to refine models, fix integration issues, and build internal confidence.

Once your pilot validates the approach, build the infrastructure to scale—better data pipelines, model monitoring systems, governance frameworks, and user training. Track ROI against your original business objectives monthly. AI systems that aren't monitored drift. Ones that are monitored improve.

The AI trends already emerging in 2026 will define competitive positioning well into the next decade.

Agentic AI: The shift from AI that answers questions to AI that takes actions. Agentic systems can autonomously execute multi-step workflows—initiating trades, processing claims, or escalating fraud alerts—without human prompts at every step.

Autonomous Financial Operations: AI will increasingly manage routine financial operations end-to-end. Reconciliation, reporting, and compliance filing will run continuously in the background with human oversight, not human execution.

AI Compliance Monitoring: Regulators are moving toward continuous compliance surveillance. AI will simultaneously help institutions meet these requirements and help regulators enforce them—a structural shift in how financial oversight works.

Hyper-Personalization at Scale: The next generation of customer AI will function as a true financial advisor for every customer—proactively guiding financial decisions based on real-time data, life events, and stated goals.

Explainable AI (XAI): Regulatory pressure and customer trust requirements are making explainability a product feature, not just a compliance checkbox. Institutions that make AI decisions transparent will build deeper customer relationships.

The future of AI in BFSI belongs to organizations that treat AI as ongoing infrastructure—not a one-time project.

General-purpose AI development firms can build impressive technology. But they often underestimate what BFSI deployment actually requires.

A specialized partner brings several things a generalist can't:

Regulatory expertise: Understanding OCC guidance on model risk management, CFPB fair lending expectations, and state insurance AI regulations isn't optional. It's foundational to building AI that survives regulatory scrutiny.

Security-first architecture: BFSI-grade AI requires SOC 2 compliance, encryption at rest and in transit, role-based access controls, and adversarial attack resistance. These aren't add-ons—they're design requirements.

BFSI-specific AI solutions: Fraud models behave differently than retail recommendation engines. Credit risk models carry legal obligations. Claims processing AI touches regulatory frameworks on multiple dimensions. Domain expertise accelerates development and reduces costly mistakes.

Long-term scalability: The right partner designs AI systems that grow with your organization—not ones that require replacement when transaction volumes double or regulatory requirements change.

SISGAIN delivers High-Impact Machine Learning Solutions built specifically for BFSI environments. Whether you need to build smart AI agents for banking automation or deploy fraud detection systems at enterprise scale, SISGAIN brings both the technical depth and regulatory understanding to deliver production-ready AI.

The difference between a demo and a deployed system is often the partner behind it.

AI is reshaping every layer of the BFSI industry—from how risk is assessed and fraud is detected, to how customers are served and compliance is maintained. The organizations pulling ahead aren't doing so because they adopted AI first. They're doing so because they adopted AI strategically.

The ten use cases covered in this article aren't experiments. They're live, revenue-generating, cost-reducing deployments running at scale across leading U.S. financial institutions right now. The technology has matured. The ROI is documented. The competitive risk of waiting is clear.

The question for BFSI leaders in 2026 isn't whether to invest in AI. It's how quickly you can do it right.

SISGAIN has the BFSI expertise, engineering depth, and regulatory understanding to help you move from strategy to deployment with confidence. Let's build something that matters.

Whether you need to reduce fraud losses, automate insurance claims, deploy banking virtual assistants, or build predictive analytics into your risk operations, SISGAIN builds the AI systems that make it happen.

Our BFSI AI capabilities include:

Start Build Your

Next Digital Solution?

Let’s build scalable, future-ready digital solutions tailored to your business goals. Connect with our experienced technology consultants to discuss your vision, strategy, and growth opportunities — with zero obligation and complete transparency.

Get a free consultation and cost estimate for your digital solution

Our expert will contact you within 24 hours. Check your email for confirmation.

Partner with SISGAIN experts to build secure, scalable AI-powered IT Solutions that transform your business operations.

DUQE FREEZONE Quarter Deck, Queen Elizabeth 2, Mina Rashid, Dubai, UAE

100 Consilium Pl Suite 200, Scarborough, ON M1H 3E3, Canada

C-109, Sector 2, Noida, Uttar Pradesh 201301 India

Project quotes, partnerships, implementation

Open roles, referrals, campus hiring